Buying a home is exciting, but let’s be honest—it can also feel overwhelming. If you’re looking into a simple mortgage in Indiana, you’re probably hoping for a straightforward way to finance a home without getting lost in complicated legal language and confusing loan terms.

The good news is that mortgages in Indiana can actually be simpler than you might think—especially when you understand how they work and what options are available. Whether you’re buying your first home, refinancing, or simply exploring your choices, this guide will walk you through everything you need to know in a clear, practical way.

Let’s break it down step by step so you can feel confident about your mortgage journey.

Table of Contents

What Is a Simple Mortgage in Indiana?

A simple mortgage in Indiana generally refers to a straightforward home loan agreement where:

- A borrower receives money to purchase property

- The property is used as collateral

- The borrower repays the loan over time with interest

In legal terms, a mortgage is a lien on a property that secures the loan. If the borrower fails to make payments, the lender has the legal right to foreclose on the property.

But don’t let the legal wording intimidate you. At its core, a mortgage is simply an agreement between you and the lender that allows you to buy a home now and pay for it gradually.

In Indiana, mortgages are commonly structured in a way that makes them fairly predictable and manageable compared to some other states.

Why Many Homebuyers Prefer a Simple Mortgage

This straightforward approach allows borrowers to understand their financial obligations clearly, making it easier to budget for monthly payments. Additionally, the predictable nature of interest rates in simple mortgages can provide peace of mind for homeowners. Many lenders also offer competitive rates, making this option appealing for first-time buyers. Ultimately, a simple mortgage can facilitate a smoother transition into homeownership by minimizing confusion and maximizing clarity.

Here are a few reasons why this approach is appealing:

1. Easy to Understand

Simple mortgages often have straightforward terms—fixed interest rates, clear payment schedules, and minimal surprises.

2. Predictable Payments

With fixed-rate mortgages, your monthly payment stays the same throughout the loan term.

3. Lower Stress

When you fully understand your mortgage terms, it reduces financial anxiety and helps you plan better.

4. Faster Approval Process

Some simple mortgage programs have fewer requirements, which can make approval quicker.

If you’re someone who values clarity and financial stability, a simple mortgage structure can make a lot of sense.

How Mortgages Work in Indiana

Before choosing a simple mortgage in Indiana, it’s helpful to understand the basics of how mortgages function in the state.

Mortgage vs. Deed of Trust

Some states use something called a deed of trust, but Indiana typically uses a mortgage system.

This means:

- The borrower keeps ownership of the property.

- The lender places a lien on the property.

- If payments stop, the lender can begin foreclosure proceedings.

Judicial Foreclosure State

Indiana is considered a judicial foreclosure state, which means foreclosure must go through the court system.

While that might sound intimidating, it actually provides borrowers with additional protections and legal oversight.

Types of Simple Mortgages Available in Indiana

Fixed-rate mortgages are a popular choice, offering consistent monthly payments over the life of the loan. Adjustable-rate mortgages, while potentially lower at the start, can fluctuate, which may lead to unexpected costs. Additionally, first-time homebuyer programs in Indiana can provide financial assistance and lower interest rates. It’s essential to shop around and compare terms from different lenders to find the best fit for your financial situation. Understanding the local market trends can also help you make an informed decision about your mortgage options.

Fixed-Rate Mortgage

This is the most straightforward type of mortgage.

Your interest rate stays the same for the entire loan period—usually 15 or 30 years.

Benefits include:

- Stable monthly payments

- Predictable budgeting

- Long-term financial security

For many buyers, this is the easiest mortgage to understand.

FHA Loans

An FHA loan is backed by the Federal Housing Administration and is popular among first-time buyers.

These loans are attractive because they typically require:

- Lower credit scores

- Smaller down payments

- Flexible approval standards

For buyers who might not qualify for traditional loans, FHA mortgages offer a simple and accessible path to homeownership.

Conventional Loans

A conventional mortgage is not backed by the government. Instead, it is issued by private lenders.

Many conventional loans offer:

- Competitive interest rates

- Flexible loan terms

- Lower long-term costs for borrowers with strong credit

If you have a good credit score and stable income, a conventional loan may be the simplest and most affordable option.

USDA Rural Housing Loans

If you’re buying a home in a rural part of Indiana, you might qualify for a USDA loan.

These loans offer a major advantage:

No down payment required.

USDA mortgages are designed to help buyers in smaller communities achieve homeownership.

Requirements for Getting a Mortgage in Indiana

These requirements typically include a minimum credit score, proof of income, and employment history. Additionally, lenders may assess your debt-to-income ratio to ensure you can manage monthly payments. First-time homebuyers often benefit from various assistance programs that can ease the financial burden. Understanding these criteria can help you prepare and increase your chances of approval for your desired mortgage type.

Most lenders evaluate these factors:

Credit Score

Your credit score helps determine your interest rate and approval odds.

Typical minimum scores:

- FHA loans: around 580

- Conventional loans: 620 or higher

Higher scores usually lead to better loan terms.

Down Payment

Your down payment depends on the type of loan.

Examples include:

- FHA loans: about 3.5%

- Conventional loans: 3%–20%

- USDA loans: 0%

The larger your down payment, the smaller your loan balance will be.

Debt-to-Income Ratio

Your debt-to-income (DTI) ratio compares your monthly debts to your income.

Most lenders prefer a DTI of 43% or lower, although some programs allow higher ratios.

Employment and Income

Lenders want to see stable income and employment history, usually for the past two years.

This helps demonstrate your ability to repay the loan.

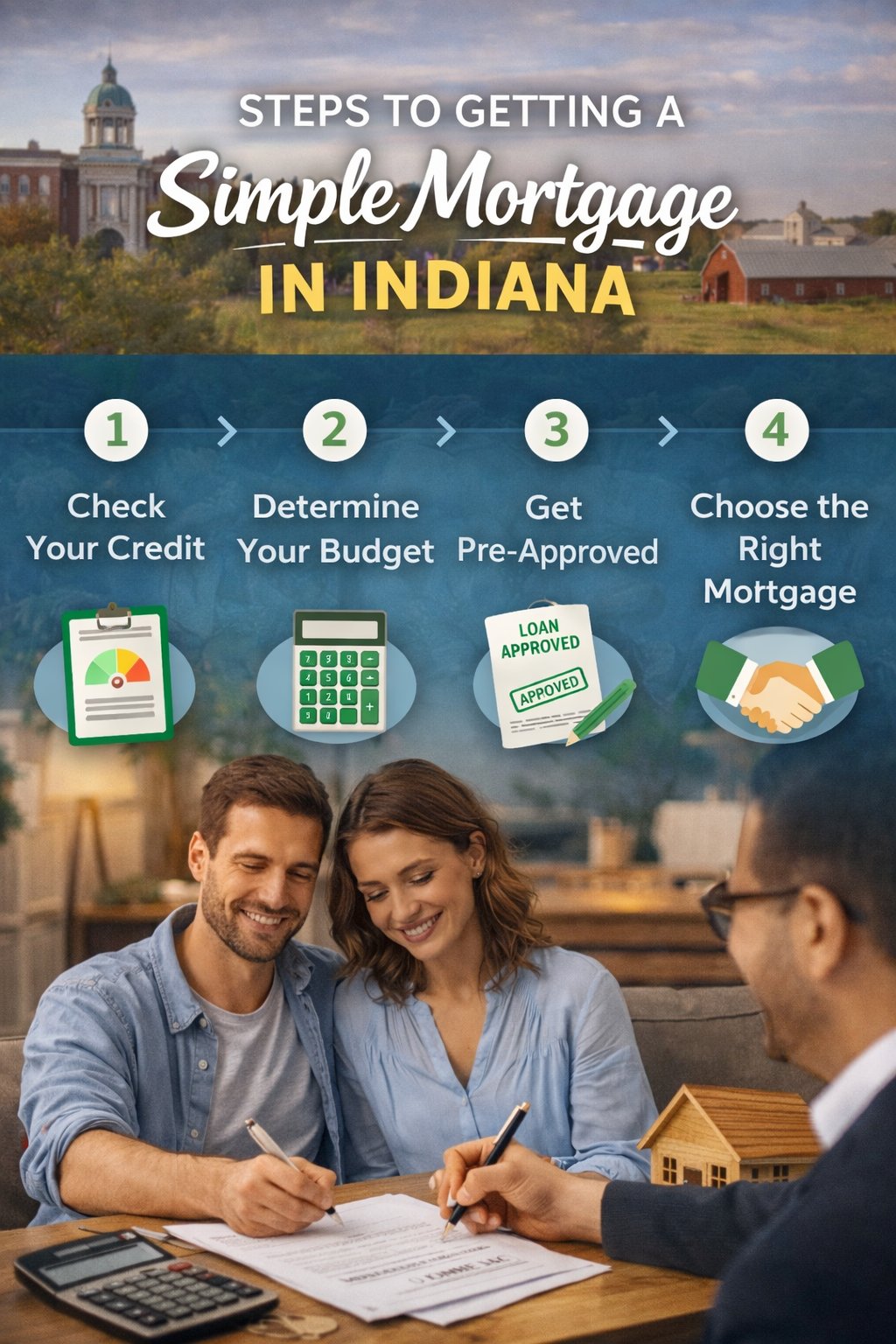

Steps to Getting a Simple Mortgage in Indiana

Start by assessing your credit score and addressing any issues that may affect it. Next, determine how much you can afford for a down payment, as this will influence your loan options. Gather necessary documentation, including proof of income and employment history, to streamline the application process. Finally, shop around for lenders to compare interest rates and terms before making a decision. By following these steps, you can increase your chances of securing a favorable mortgage.

Step 1: Check Your Credit

Before applying for a mortgage, review your credit report and score.

If your score needs improvement, paying down debts and avoiding new credit inquiries can help.

Step 2: Determine Your Budget

A mortgage lender may approve you for a certain amount, but that doesn’t always mean it fits comfortably into your budget.

Consider:

- Monthly mortgage payments

- Property taxes

- Home insurance

- Maintenance costs

Step 3: Get Pre-Approved

Mortgage pre-approval shows sellers that you are a serious buyer.

It also helps you understand:

- Your borrowing limit

- Your estimated interest rate

- Your monthly payment range

Step 4: Choose the Right Mortgage

Look for a mortgage that is:

- Easy to understand

- Affordable long term

- Suitable for your financial situation

Many buyers prefer a fixed-rate mortgage because it keeps things simple.

Step 5: Close on Your Home

Closing is the final step in the mortgage process.

During closing you will:

- Sign mortgage documents

- Pay closing costs

- Receive the keys to your home

Once everything is complete, your mortgage payments officially begin.

Understanding Closing Costs in Indiana

Start by assessing your credit score and addressing any issues that may affect it. Next, determine how much you can afford for a down payment, as this will influence your loan options. Gather necessary documentation, including proof of income and employment history, to streamline the application process. Finally, shop around for lenders to compare interest rates and terms before making a decision. By following these steps, you can increase your chances of securing a favorable mortgage.

Typical closing costs include:

- Loan origination fees

- Title search fees

- Appraisal costs

- Attorney fees

- Recording fees

In Indiana, closing costs typically range from 2% to 5% of the home price.

While this may seem like a lot, some lenders allow these costs to be negotiated or rolled into the mortgage.

Tips for Getting the Best Mortgage in Indiana

Consider getting pre-approved for a mortgage to understand your budget better and show sellers that you are a serious buyer. Additionally, maintaining a good credit score can lead to better loan terms and lower interest rates. It’s also beneficial to consult with a real estate agent who understands the local market and can provide valuable insights. Remember to review all loan documents carefully before signing to ensure you understand your obligations. Taking these steps can help you navigate the home-buying process more effectively.

Here are some practical tips.

Improve Your Credit Score

Even a small increase in your credit score can reduce your interest rate and save thousands over the life of your loan.

Simple ways to boost your score include:

- Paying bills on time

- Reducing credit card balances

- Avoiding new debt before applying

Shop Around for Lenders

Not all lenders offer the same rates or terms.

Getting quotes from multiple lenders can help you find the best deal.

A small difference in interest rate can significantly affect your monthly payment.

Consider Loan Terms Carefully

A 30-year mortgage offers lower monthly payments, while a 15-year mortgage saves money on interest.

Think about what fits best with your long-term financial goals.

Save for a Larger Down Payment

The more money you put down upfront, the less you’ll need to borrow.

Benefits include:

- Lower monthly payments

- Better loan terms

- Less interest over time

Common Mistakes to Avoid

When searching for a simple mortgage in Indiana, it’s easy to make mistakes that could cost you money or delay the process.

Here are a few things to watch out for.

Taking on New Debt

Avoid financing a car or opening new credit cards before closing on your home.

New debt can affect your mortgage approval.

Skipping the Pre-Approval Step

House hunting without pre-approval can lead to disappointment if you fall in love with a home outside your budget.

Ignoring Hidden Costs

Homeownership includes more than just mortgage payments.

Be sure to account for:

- Property taxes

- Insurance

- Repairs

- Utilities

Is a Simple Mortgage Right for You?

Consider your long-term financial goals when deciding on the terms of your mortgage. Understanding interest rates and how they impact your monthly payments is crucial. Research different lenders to find the best rates and terms that suit your needs. Additionally, always read the fine print to avoid unexpected fees or penalties. Finally, consult with a financial advisor to ensure that you are making an informed decision that aligns with your financial situation.

It’s especially beneficial for:

- First-time homebuyers

- Buyers who prefer predictable payments

- People who want straightforward loan terms

If you value simplicity and financial transparency, choosing a clear and easy-to-understand mortgage structure can make your homeownership journey much smoother.

Final Thoughts

Getting a simple mortgage in Indiana doesn’t have to be complicated. When you understand the basics—loan types, requirements, and the application process—you can navigate the mortgage world with confidence.

Take your time researching lenders, improving your credit, and choosing a loan that fits your budget and lifestyle.

Buying a home is more than just a financial investment—it’s about creating a place where your life happens. With the right mortgage strategy, you’ll be well on your way to making that dream a reality.

If you’re starting your home search in Indiana, remember: the best mortgage isn’t always the most complex one. Sometimes, the simplest option is the smartest choice.