Real estate financing can involve many different legal structures, some of which date back centuries. One such structure is the English mortgage, a concept rooted in traditional property law that still influences modern lending and mortgage arrangements. While many borrowers in the United States are more familiar with conventional mortgages, the English mortgage remains an important legal concept, especially when discussing property rights, security interests, and lender protections.

For property owners, investors, and legal professionals in Indiana, understanding the English mortgage can help clarify how property can be used as collateral, how ownership rights are structured during a loan, and how foreclosure processes may unfold if obligations are not met.

This article explores the English mortgage in Indiana, covering its legal foundations, structure, differences from other mortgage types, advantages, risks, and how it fits within Indiana’s real estate and lending environment.

Table of Contents

What Is an English Mortgage?

An English mortgage is a type of mortgage arrangement in which the borrower transfers absolute ownership of the property to the lender as security for a loan, with the condition that ownership will be transferred back to the borrower once the loan is fully repaid.

In simpler terms, the borrower temporarily gives legal title of the property to the lender. Once the borrower fulfills the repayment obligations, the lender is required to return ownership of the property to the borrower.

Key elements of an English mortgage include:

- Transfer of property ownership to the lender

- A promise by the borrower to repay the loan on a specified date

- An agreement that the lender will reconvey the property once the debt is satisfied

Although the concept originated in English property law, its influence has extended into many common law jurisdictions, including the United States.

Historical Background of the English Mortgage

The English mortgage dates back to medieval England when lenders required strong assurances that loans secured by land would be repaid. During that time, land ownership was the most reliable form of wealth and collateral.

The early mortgage system was extremely strict. If a borrower failed to repay the loan by the agreed date, the lender could permanently retain ownership of the land.

Over time, courts recognized that this system could be unfair to borrowers. As a result, the equity of redemption principle was developed. This principle allowed borrowers to reclaim their property even after the repayment deadline, provided the loan was ultimately paid.

This concept became a cornerstone of modern mortgage law and continues to influence mortgage practices today.

How English Mortgages Work

To better understand the English mortgage structure, it helps to look at the typical process.

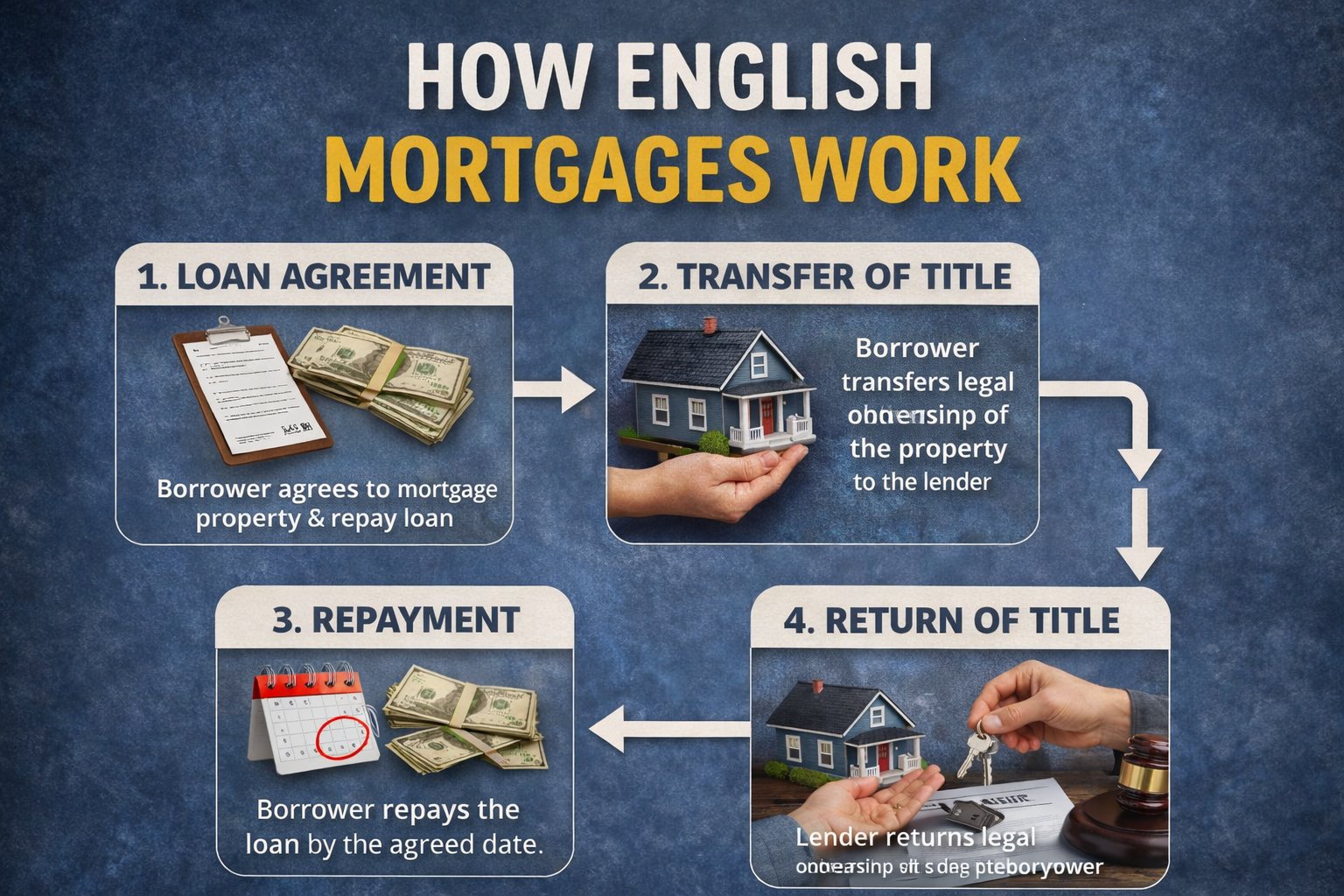

1. Loan Agreement

The borrower and lender agree on a loan amount, interest rate, and repayment date. The borrower offers property as collateral for the loan.

2. Transfer of Title

Under an English mortgage, the borrower transfers legal ownership of the property to the lender.

However, this transfer is conditional. The agreement specifies that the property will be transferred back to the borrower once the loan is repaid.

3. Borrower Retains Possession

Even though the lender technically holds title, the borrower typically remains in possession of the property and continues to use it.

4. Repayment

If the borrower repays the loan according to the agreement, the lender must transfer the title back to the borrower.

5. Default

If the borrower fails to repay the loan, the lender can exercise ownership rights over the property and may sell it to recover the debt.

English Mortgage vs. Conventional Mortgage

In modern U.S. real estate transactions, most mortgages function differently from the traditional English mortgage.

The key distinction lies in ownership of the property.

Conventional Mortgage

In a conventional mortgage:

- The borrower retains legal ownership of the property.

- The lender receives a lien on the property as security.

This lien allows the lender to foreclose if the borrower fails to repay the loan.

English Mortgage

In an English mortgage:

- Legal ownership temporarily transfers to the lender.

- The borrower regains ownership once the debt is repaid.

While the practical outcomes may sometimes appear similar, the legal structures are fundamentally different.

Mortgage Law in Indiana

Indiana is considered a lien theory state when it comes to mortgages.

This means that in most standard mortgage arrangements:

- The borrower retains legal title to the property.

- The lender holds a lien against the property.

Because of this structure, the classic English mortgage format is not commonly used in Indiana residential lending. However, understanding the concept remains valuable in several contexts, including:

- Legal analysis

- Historical property law

- Certain private financing arrangements

- Academic study of mortgage structures

Indiana law generally governs mortgage transactions through statutes and case law that focus on liens, foreclosure rights, and borrower protections.

Foreclosure Process in Indiana

When a borrower fails to repay a mortgage loan in Indiana, the lender must follow the judicial foreclosure process.

This process includes several stages.

Filing a Lawsuit

The lender must file a foreclosure lawsuit in court to begin the process.

Court Review

A judge reviews the case to determine whether the lender has the legal right to foreclose.

Judgment

If the court rules in favor of the lender, it will issue a foreclosure judgment.

Sheriff’s Sale

The property is then sold at a public auction known as a sheriff’s sale.

Redemption Period

Indiana typically allows a redemption period, giving the borrower an opportunity to reclaim the property under certain circumstances.

Even though Indiana uses lien theory rather than title transfer like an English mortgage, the foreclosure process ultimately serves a similar purpose: allowing the lender to recover the debt using the property as collateral.

Legal Principles Behind English Mortgages

Several legal principles underpin the English mortgage system.

Equity of Redemption

The borrower retains the right to reclaim the property once the loan is repaid.

This principle protects borrowers from permanently losing property due to minor repayment delays.

Security Interest

The primary purpose of the mortgage is to secure repayment of the loan.

Even when legal title is transferred, the underlying goal remains debt security.

Conditional Ownership

The lender’s ownership is conditional and tied directly to the borrower’s repayment obligations.

Situations Where English Mortgage Concepts May Appear in Indiana

Although Indiana typically follows lien theory, elements similar to English mortgage concepts may appear in certain legal arrangements.

Private Real Estate Financing

Some private lenders may structure agreements in ways that resemble title transfer arrangements.

Deeds of Trust

While Indiana primarily uses mortgages rather than deeds of trust, understanding title-based security structures can help interpret similar arrangements used in other states.

Legal Education

Law students and attorneys often study the English mortgage to understand the evolution of modern mortgage law.

International Real Estate Transactions

Investors involved in international property markets may encounter English mortgages in jurisdictions where they remain more common.

Advantages of the English Mortgage Structure

Historically, the English mortgage offered several benefits to lenders.

Strong Security for Lenders

Since legal title is transferred to the lender, the lender has strong protection against borrower default.

Simplified Enforcement

In theory, lenders could enforce repayment more easily because they already held legal ownership of the property.

Clear Legal Framework

The conditional ownership structure created a straightforward legal relationship between borrower and lender.

Risks and Disadvantages

Despite its strengths, the English mortgage also carries risks and drawbacks.

Borrower Risk

Borrowers face a higher risk because legal ownership of their property transfers to the lender during the loan period.

Potential for Abuse

Historically, lenders could exploit strict repayment deadlines to permanently acquire valuable property.

Legal Complexity

Modern mortgage systems often prefer lien-based structures because they provide clearer borrower protections.

Why the U.S. Moved Away from English Mortgages

The American mortgage system evolved to provide greater protection for borrowers.

Several factors contributed to the shift away from title transfer mortgages.

Consumer Protection

Modern mortgage laws aim to prevent borrowers from losing property unfairly.

Regulatory Framework

Federal and state regulations now govern mortgage lending practices.

Judicial Oversight

Foreclosure processes often require court involvement to ensure fairness.

As a result, most U.S. states—including Indiana—adopted lien theory or hybrid mortgage systems.

Practical Implications for Indiana Homeowners

For most homeowners in Indiana, the English mortgage is primarily a legal concept rather than a common practice.

However, understanding the idea can still be helpful.

Real Estate Education

Learning about historical mortgage systems can provide valuable insight into modern property law.

Legal Awareness

Borrowers should always understand the legal structure of any loan secured by real estate.

Private Lending

In rare cases, unconventional financing agreements may resemble older mortgage structures.

Tips for Borrowers in Indiana

When dealing with any mortgage arrangement, borrowers should take several precautions.

Read Loan Agreements Carefully

Understanding the terms of a mortgage agreement is essential before signing any documents.

Consult Legal Professionals

Real estate attorneys can explain the legal implications of mortgage agreements.

Verify Lender Credentials

Borrowers should ensure lenders are properly licensed and reputable.

Understand Foreclosure Risks

Missing payments can eventually lead to foreclosure, even under modern mortgage systems.

Tips for Real Estate Investors

Investors working in Indiana’s real estate market should also understand mortgage structures.

Study Local Laws

Indiana’s lien theory system governs most property financing.

Evaluate Financing Options

Different financing arrangements may provide varying levels of risk and flexibility.

Work With Experienced Professionals

Real estate attorneys and mortgage advisors can help investors structure secure transactions.

The Future of Mortgage Structures

Mortgage law continues to evolve as financial markets and legal frameworks change.

New financing methods, such as digital mortgages and blockchain-based property records, may reshape how property security interests are recorded and enforced.

However, the core principles that originated with early systems like the English mortgage—using property as collateral for debt—remain central to real estate finance.

Conclusion

The English mortgage represents one of the earliest and most influential forms of property-based lending. While it originated in English law and involved transferring legal title of property to lenders, its concepts helped shape the modern mortgage systems used today.

In Indiana, most mortgages operate under the lien theory system, meaning borrowers retain ownership while lenders hold a security interest in the property. Even so, understanding the English mortgage provides valuable insight into the historical development of mortgage law and the legal principles that continue to govern real estate financing.

For homeowners, investors, and legal professionals, learning about the English mortgage can deepen their understanding of property rights, lending structures, and the evolution of real estate law in the United States.

As the real estate market continues to evolve, these foundational concepts remain essential knowledge for anyone involved in property ownership or real estate finance.