When most people hear the word mortgage, they imagine a bank loan, stacks of paperwork, and a formal agreement recorded with the county. But in Indiana, there’s another concept that can create mortgage-like rights—even without a traditional mortgage document. It’s called an equitable mortgage.

If you’re a homeowner, real estate investor, private lender, or someone dealing with property disputes, understanding equitable mortgage in Indiana can protect you from serious legal and financial issues. In some cases, a deal you thought was simple may legally become a mortgage—even if you never called it one.

In this guide, we’ll break everything down in plain English. You’ll learn what an equitable mortgage is, how Indiana courts interpret it, when it applies, and what you should do if you’re involved in a situation that might qualify as one.

Table of Contents

What Is an Equitable Mortgage?

An equitable mortgage is a legal concept where a transaction that wasn’t formally structured as a mortgage is treated like a mortgage by a court.

In simple terms:

If a property transfer or agreement was intended to secure repayment of a debt, Indiana courts may treat it as a mortgage—even if the documents say otherwise.

This doctrine exists to prevent unfair situations where someone tries to disguise a loan as something else, such as:

- A property sale

- A deed transfer

- A lease agreement

- A land contract

If the real purpose of the transaction was to secure a loan, the court may declare it an equitable mortgage.

This protects borrowers from losing property unfairly and ensures lenders follow proper foreclosure procedures.

Why Equitable Mortgages Exist

The idea behind this mortgages comes from equity law, which focuses on fairness rather than just strict legal technicalities.

Without this rule, lenders could potentially bypass foreclosure laws by structuring deals like this:

- “Sell me your house for $50,000.”

- “You can buy it back later if you repay me.”

If the homeowner actually borrowed $50,000 and the property transfer was only meant as collateral, courts may treat it as a mortgage instead of a sale.

Indiana courts look at the true intent of the parties, not just the paperwork.

How Indiana Courts Define an Equitable Mortgage

In Indiana, courts analyze several factors to determine whether a transaction qualifies as an equitable mortgage.

They typically ask:

- Was there a debt or loan involved?

- Was the property intended to secure repayment?

- Did the borrower maintain possession or control of the property?

- Was the property worth significantly more than the amount paid?

- Did the agreement allow the borrower to repurchase the property?

If the answers suggest the deal was meant to secure a loan, the court may rule that this mortgage exists.

The key principle is simple:

Substance matters more than form.

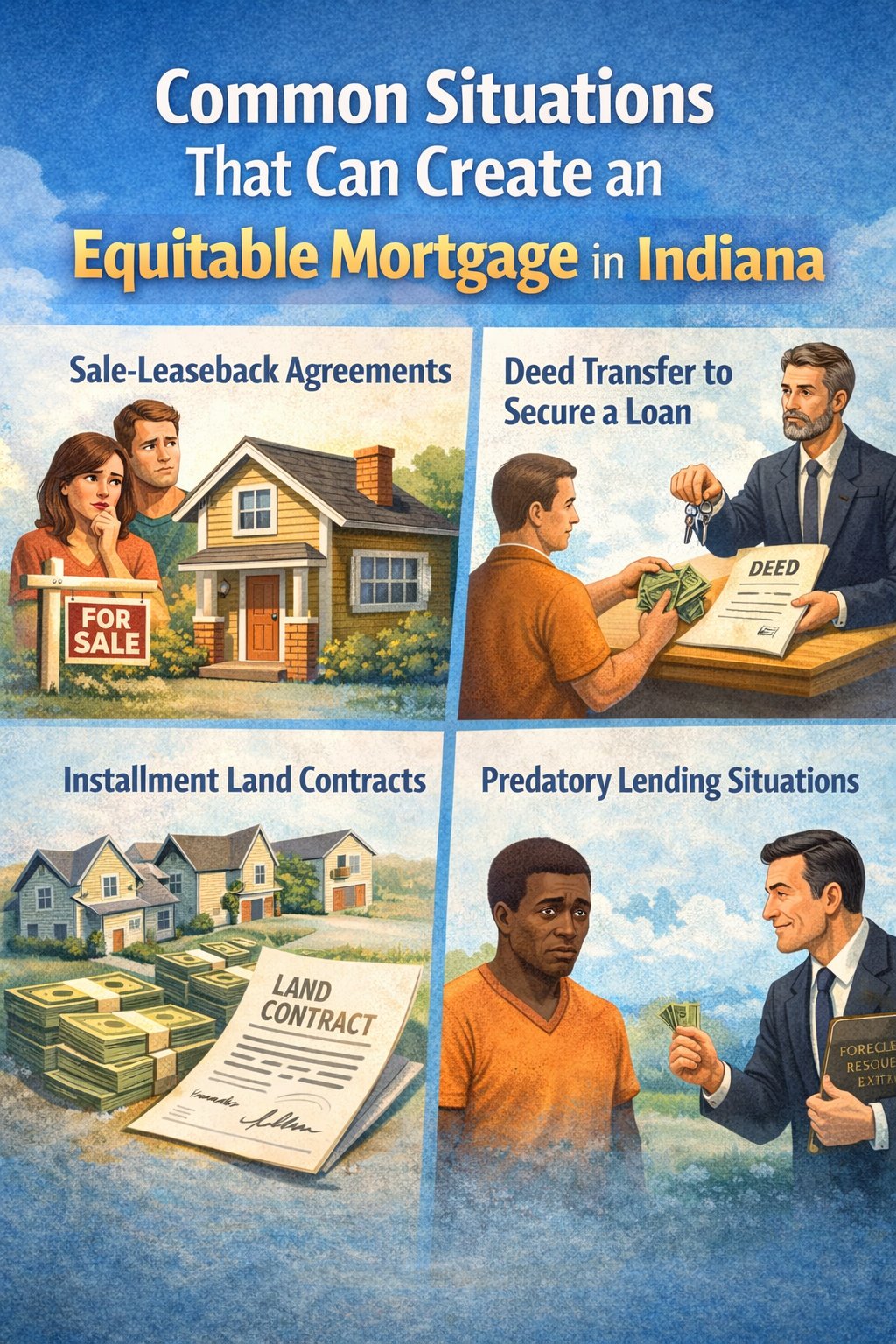

Common Situations That Can Create an Equitable Mortgage in Indiana

Many people are surprised to learn how often this mortgage disputes occur. Here are several situations where Indiana courts may apply this doctrine.

1. Sale-Leaseback Agreements

In a sale-leaseback, a homeowner sells their property and immediately leases it back.

These arrangements are sometimes used by investors offering quick cash to distressed homeowners.

However, if the homeowner was actually borrowing money and the sale was meant only as security, courts may treat the agreement as this mortgage.

2. Deed Transfers to Secure a Loan

Sometimes borrowers transfer the deed to a lender as “security” instead of creating a formal mortgage.

For example:

- A borrower needs $30,000 quickly

- The lender asks for the deed as collateral

- The borrower agrees to repay within 12 months

Even if the document says it’s a sale, a court may recognize it as an equitable mortgage.

3. Installment Land Contracts

Some land contracts resemble mortgages but are structured differently.

If the buyer effectively acts like the homeowner and is paying toward ownership, courts may interpret the contract as a mortgage-like arrangement.

4. Predatory Lending Situations

This mortgage claims often arise when vulnerable homeowners are targeted by investors offering:

- quick cash

- foreclosure rescue

- debt relief

If the transaction was structured unfairly, courts may intervene.

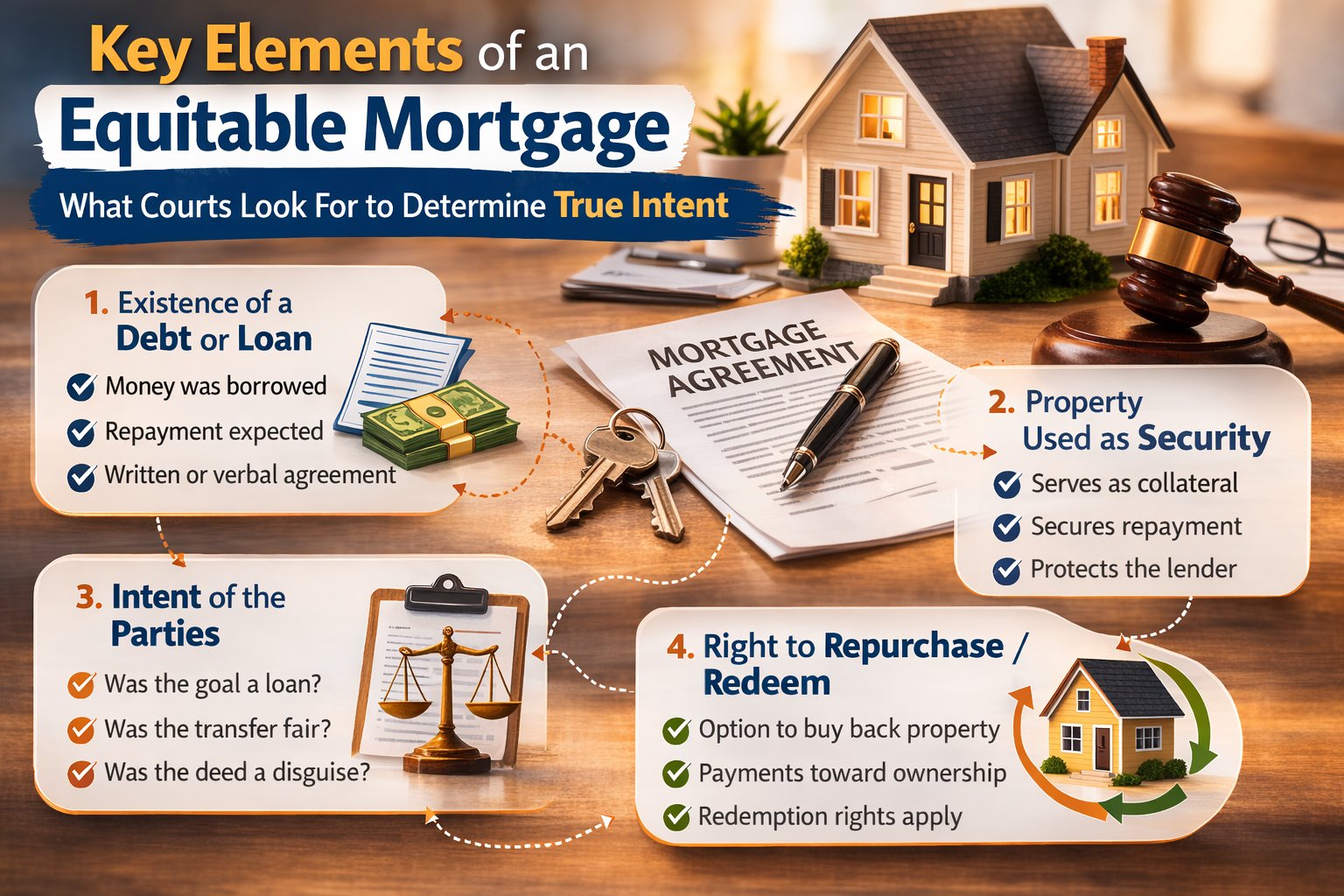

Key Elements of an Equitable Mortgage

To establish this mortgage in Indiana, courts usually look for these essential elements.

1. A Debt Must Exist

The most important factor is the presence of a loan or obligation.

If no debt exists, the court is unlikely to treat the transaction as a mortgage.

2. Property Used as Security

The property must have been intended as collateral for the debt.

This can be shown through:

- written agreements

- verbal promises

- payment records

- surrounding circumstances

3. Intent of the Parties

Indiana courts heavily examine the intent behind the transaction.

Even if documents describe the transaction as a sale, the court may ignore the label if the true intent was security for a loan.

Real Example of How an Equitable Mortgage Works

Imagine this situation.

Sarah is facing foreclosure and needs quick money.

An investor offers her this deal:

- He pays Sarah $40,000

- She signs a deed transferring ownership

- She can buy the house back within two years for $55,000

The house is worth $180,000.

Sarah continues living in the home and pays monthly payments.

If a dispute arises, a court may determine:

- The investor actually made a loan

- The deed was meant as security

- The transaction is an equitable mortgage

Instead of losing the home automatically, the investor would have to foreclose like a normal mortgage lender.

This protects Sarah’s rights.

Why Equitable Mortgages Matter for Indiana Homeowners

Understanding equitable mortgages can protect homeowners in several ways.

Protection Against Hidden Loans

Sometimes agreements that appear to be sales are actually disguised loans.

The equitable mortgage doctrine prevents lenders from taking property without foreclosure protections.

Right to Redemption

If a transaction is declared an equitable mortgage, the borrower may gain the right to redeem the property by repaying the debt.

Foreclosure Requirements

Lenders must follow Indiana foreclosure laws instead of simply taking the property.

This gives homeowners more time and legal protections.

Risks for Lenders and Investors

Private lenders and real estate investors also need to understand equitable mortgage rules.

If a court reclassifies a deal as a mortgage, it can dramatically change the outcome.

You May Be Forced to Foreclose

Instead of owning the property outright, you may have to go through a lengthy foreclosure process.

Interest and Lending Laws Apply

Certain lending regulations may apply retroactively.

Legal Disputes Can Be Expensive

This mortgage cases often involve complex litigation.

Investors who structure deals improperly may face lawsuits.

How Courts Determine Intent

Determining intent is one of the most challenging parts of this mortgage cases.

Indiana courts evaluate multiple factors, including:

- the relationship between the parties

- financial distress of the borrower

- fairness of the purchase price

- who maintained possession of the property

- payment arrangements

- written and verbal communications

Courts may also consider whether the borrower had access to legal advice when entering the agreement.

Signs a Transaction Might Be an Equitable Mortgage

If you’re involved in a property deal, watch for these warning signs.

A transaction might be treated as this mortgage if:

- The borrower still lives in the home

- Payments resemble loan repayments

- The buyer paid far less than market value

- There is an option to repurchase the property

- The transaction was intended to secure repayment

If several of these factors exist, the deal may attract legal scrutiny.

Indiana Case Law on Equitable Mortgages

Indiana courts have recognized this mortgages for many years.

The general legal principle is that:

A deed absolute in form may be considered a mortgage if it was intended to secure a debt.

Courts analyze the totality of circumstances rather than relying on a single factor.

This flexible approach helps prevent unfair outcomes.

How to Avoid Equitable Mortgage Disputes

Whether you are a homeowner or investor, clear documentation is the best protection.

Here are some practical tips.

Use Proper Mortgage Documents

If money is being loaned against property, use a promissory note and recorded mortgage.

Avoid informal arrangements.

Get Independent Legal Advice

Both parties should consult attorneys before signing complex real estate agreements.

Ensure Fair Market Value

If a property is sold, the purchase price should reflect the property’s actual value.

Large discrepancies raise red flags.

Avoid “Foreclosure Rescue” Schemes

Homeowners facing foreclosure should be cautious when investors offer fast cash deals.

Some of these arrangements later become equitable mortgage disputes.

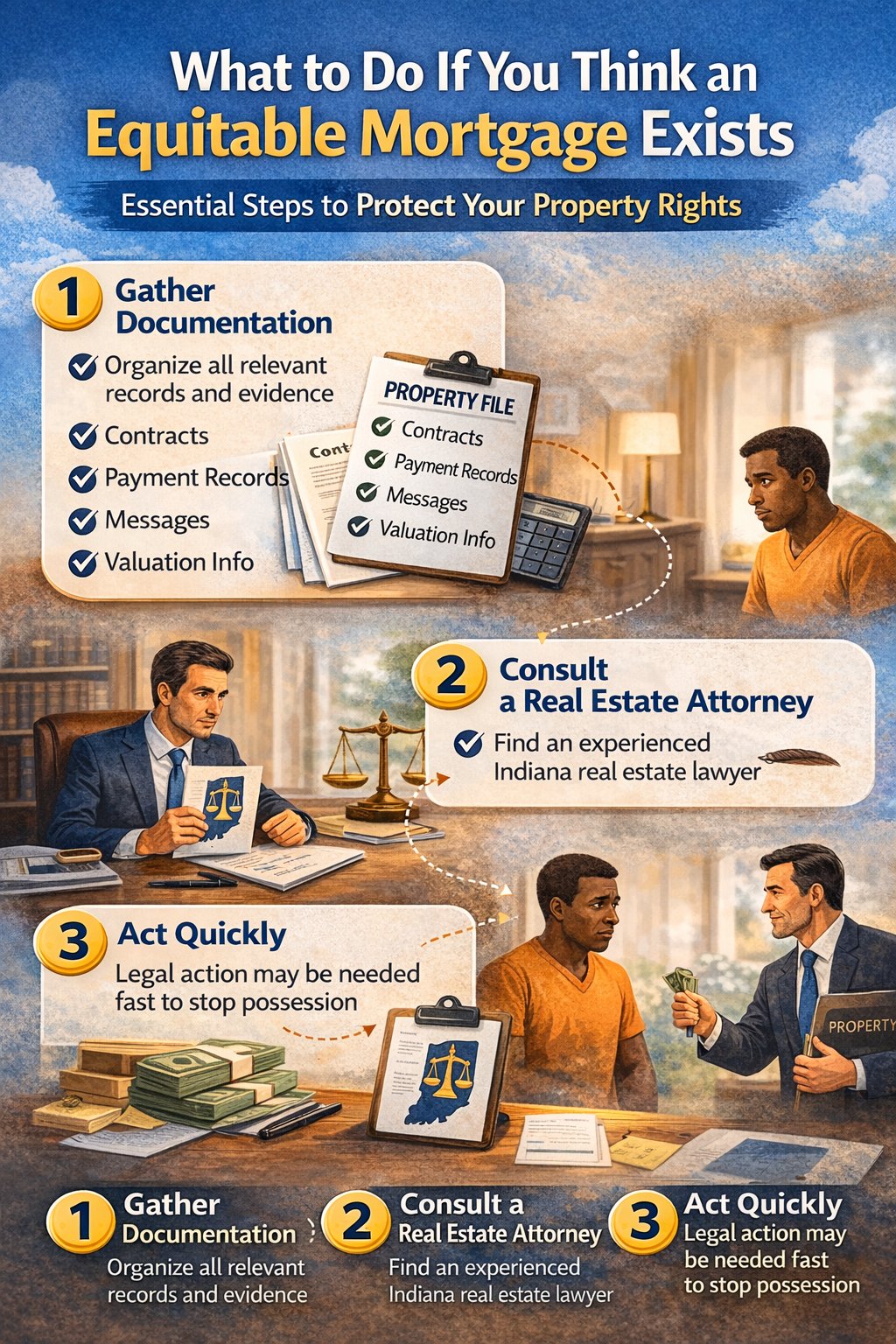

What to Do If You Think an Equitable Mortgage Exists

If you believe a transaction involving your property may qualify as an equitable mortgage, consider taking these steps.

1. Gather Documentation

Collect all relevant materials, including:

- contracts

- payment records

- emails or text messages

- property valuation information

2. Consult a Real Estate Attorney

This mortgage cases are highly fact-specific.

A knowledgeable Indiana real estate attorney can evaluate your situation.

3. Act Quickly

If a lender or investor is attempting to take possession of the property, legal action may be necessary.

Waiting too long can weaken your position.

Frequently Asked Questions About Equitable Mortgage in Indiana

Is an equitable mortgage legally enforceable?

Yes. Courts can enforce equitable mortgages even when no formal mortgage document exists.

Can a deed be considered a mortgage?

Yes. If the deed was intended to secure a loan, courts may treat it as a mortgage.

Does the agreement have to be written?

Not necessarily. Courts may rely on surrounding circumstances and conduct.

Can homeowners recover property through equitable mortgage claims?

In some cases, yes. If a transaction is deemed an equitable mortgage, the borrower may regain rights to redeem the property.

Final Thoughts: Why Understanding Equitable Mortgage in Indiana Matters

Real estate transactions are often more complicated than they appear. The concept of an equitable mortgage in Indiana reminds us that courts care about fairness and intent, not just paperwork.

If a deal involving property was really meant to secure a loan, Indiana courts may treat it as a mortgage—even if the documents say otherwise.

For homeowners, this rule provides protection from unfair or deceptive property transfers. For lenders and investors, it serves as a reminder to structure transactions carefully and transparently.

If you’re ever unsure about a property agreement, getting professional legal guidance early can save significant time, money, and stress.

Key Takeaway:

When property is used as security for a loan, Indiana courts may recognize an equitable mortgage, ensuring borrowers receive the same legal protections as traditional mortgages.

Understanding this concept can help you avoid costly mistakes and make smarter real estate decisions.