Buying a home is rarely just a financial decision—it’s emotional, personal, and often a little overwhelming. If you’re exploring your mortgage options in Indiana, chances are you’ve come across something called a Hybrid ARM mortgage and wondered: Is this actually a smart move for me?

This guide is designed to walk you through everything you need to know about Hybrid Adjustable-Rate Mortgages (ARMs) in Indiana—in plain, human language. No jargon overload. No sales pressure. Just clarity.

Table of Contents

What Is a Hybrid ARM Mortgage?

Let’s start simple.

A Hybrid ARM (Adjustable-Rate Mortgage) is a home loan that combines two phases:

- A fixed-rate period (where your interest rate doesn’t change)

- An adjustable-rate period (where your rate can go up or down)

Think of it as the “best of both worlds” mortgage—at least on the surface.

During the first phase, your monthly payments are predictable and stable. After that, your rate adjusts periodically based on market conditions.

How Hybrid ARMs Actually Work

Hybrid ARMs are usually written like this:

- 5/1 ARM

- 7/1 ARM

- 10/1 ARM

Here’s what that means:

- The first number = how long your rate is fixed

- The second number = how often it adjusts afterward

So, a 5/1 ARM means:

- Fixed rate for 5 years

- Adjusts every year after that

This structure gives you breathing room early on—but requires planning for the future.

Why Hybrid ARMs Are Popular in Indiana

Indiana has a unique housing landscape:

- Lower home prices compared to national averages

- Strong first-time buyer market

- Growing suburban and mid-sized city demand

Because of this, Hybrid ARMs often appeal to buyers who:

- Want lower initial monthly payments

- Expect to move within 5–10 years

- Plan to refinance later

- Anticipate income growth

And here’s the key: Hybrid ARMs typically offer lower initial interest rates than fixed mortgages, which can make homeownership more accessible upfront.

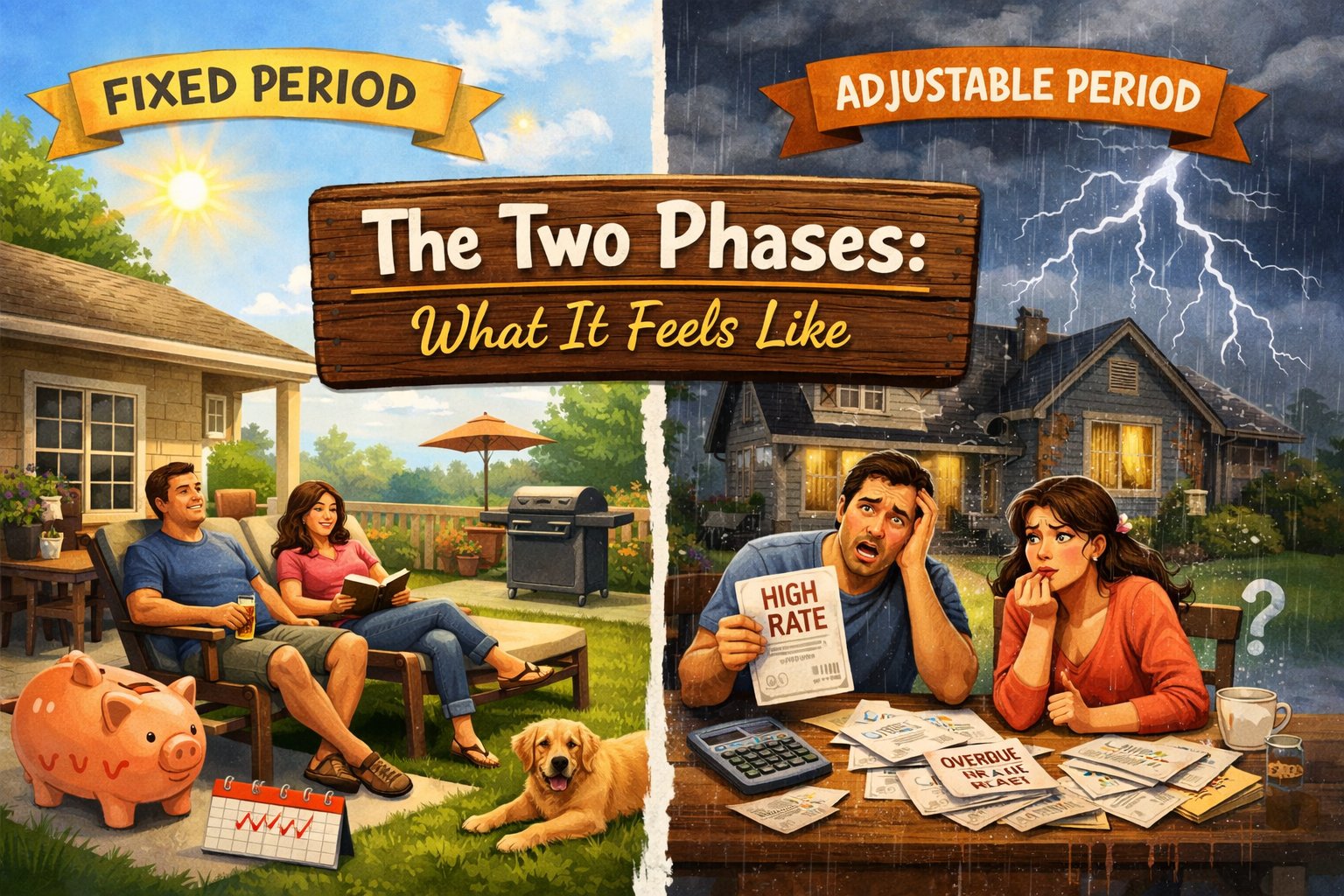

The Two Phases: What It Feels Like

Phase 1: The “Comfort Zone”

This is your fixed-rate period.

- Your payments are stable

- Your interest rate doesn’t change

- Budgeting is easy

For many Indiana homeowners, this phase feels safe and predictable—especially in the first few years of homeownership.

Phase 2: The “Unknown Zone”

After the fixed period ends, your rate adjusts.

This adjustment is based on:

- A market index (like Treasury rates)

- A lender’s margin

So your new rate = index + margin

And yes—your payment can go up.

Or down.

But let’s be honest: most people worry about it going up.

The Big Advantage: Lower Starting Payments

One of the biggest reasons people choose a Hybrid ARM is simple:

Lower monthly payments in the beginning.

Compared to a traditional 30-year fixed mortgage, Hybrid ARMs often start with a lower interest rate.

That can mean:

- More affordable entry into homeownership

- Ability to buy a slightly better home

- Extra room in your monthly budget

For young professionals in Indianapolis, Fort Wayne, or Bloomington, this can be a game changer.

But There’s a Catch (Of Course)

Nothing in real estate is ever one-sided.

The trade-off for that lower initial rate is uncertainty later.

After your fixed period:

- Your rate can increase

- Your payment can rise

- Your long-term cost may be higher

That’s why Hybrid ARMs are often best for people who don’t plan to stay in the home long-term.

Who Should Consider a Hybrid ARM in Indiana?

Let’s get real. This isn’t for everyone.

A Hybrid ARM might be a great fit if you:

1. Plan to Move Soon

If you’re likely to sell within 5–10 years, you may never even reach the adjustable phase.

2. Expect Your Income to Grow

Maybe you’re early in your career, and you anticipate higher earnings in the future.

3. Want to Maximize Cash Flow Now

Lower payments today can help you:

- Invest

- Save

- Pay off other debt

4. Are Comfortable With Some Risk

This isn’t a “set it and forget it” mortgage. It requires awareness and planning.

Who Should Probably Avoid It?

Let’s be just as honest on the other side.

A Hybrid ARM may not be ideal if you:

- Plan to stay in your home long-term (15–30 years)

- Want predictable payments forever

- Are on a tight or fixed budget

- Lose sleep over financial uncertainty

In those cases, a fixed-rate mortgage might give you more peace of mind.

Understanding Rate Adjustments (Without the Headache)

When your rate adjusts, it’s not random.

There are safeguards called caps, which limit how much your rate can increase:

- Initial cap – first adjustment limit

- Periodic cap – limits each adjustment

- Lifetime cap – maximum increase over the loan

For example, a 2/2/5 cap means:

- First adjustment: max +2%

- Each following adjustment: max +2%

- Total increase: max +5%

These caps protect you from extreme spikes—but they don’t eliminate risk entirely.

Real-Life Scenario: Indiana Buyer

Let’s make this real.

Meet Jake from Indianapolis:

- Buys a $250,000 home

- Chooses a 5/1 ARM

- Gets a lower initial rate than a 30-year fixed

For 5 years:

- His payments are manageable

- He saves money monthly

By year 5:

- He gets a promotion

- His income increases

- He refinances into a fixed loan

Result? He benefited from the ARM without facing the risk.

Now compare that to someone who:

- Stays past the fixed period

- Faces rising interest rates

- Hasn’t planned ahead

That’s where problems can begin.

Hybrid ARM vs Fixed Mortgage (Quick Comparison)

| Feature | Hybrid ARM | Fixed Mortgage |

|---|---|---|

| Initial Rate | Lower | Higher |

| Payment Stability | Temporary | Permanent |

| Risk Level | Medium–High | Low |

| Best For | Short-term owners | Long-term owners |

Indiana-Specific Considerations

While mortgage products are largely standardized across the U.S., your local housing market matters.

In Indiana:

- Property taxes are relatively moderate

- Home values are more stable than volatile markets

- Many buyers stay 5–10 years before moving

This actually aligns well with Hybrid ARM timelines.

But you still need to factor in:

- Local job stability

- Regional economic growth

- Personal life plans

The Emotional Side of This Decision

Let’s pause for a moment.

Choosing a mortgage isn’t just math.

It’s about:

- Security

- Stability

- Peace of mind

Some people love the flexibility of a Hybrid ARM.

Others hate the idea of uncertainty—even if it saves money.

Neither is wrong.

The right choice is the one that lets you sleep at night.

Common Misconceptions

“Hybrid ARMs are risky loans.”

Not necessarily. They’re just different. The risk depends on how you use them.

“Rates will definitely go up.”

Not always. They can go down too—but you shouldn’t rely on that.

“They’re only for experts.”

Nope. Many first-time buyers use them—successfully.

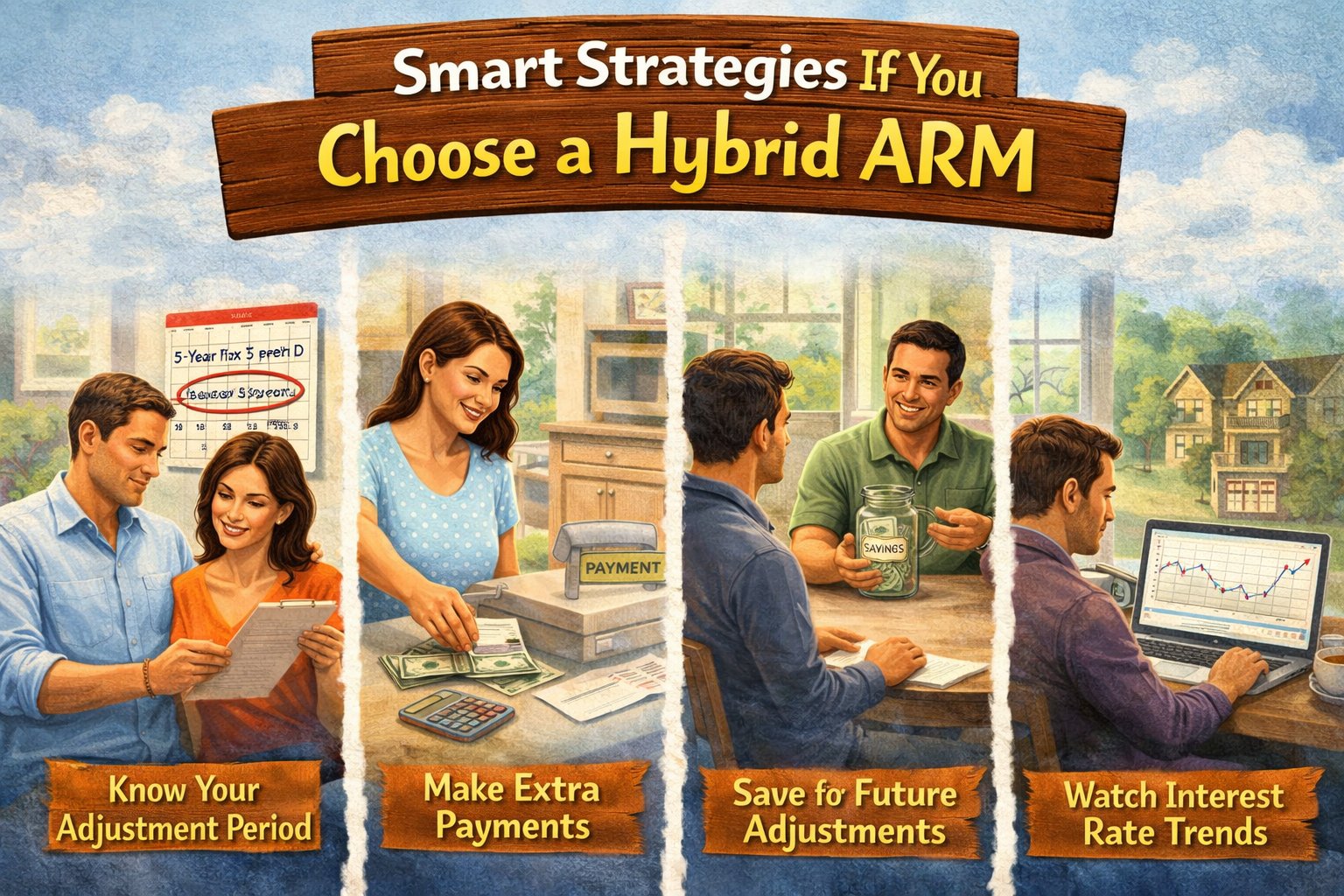

Smart Strategies If You Choose a Hybrid ARM

If you’re leaning toward this option, here’s how to do it wisely:

1. Plan Your Exit Strategy

Will you:

- Sell?

- Refinance?

- Pay down aggressively?

Have a plan before you sign.

2. Build a Financial Cushion

Save extra during the fixed period.

Future you will thank you.

3. Understand Your Loan Terms

Know your:

- Caps

- Index

- Adjustment schedule

Don’t skip the fine print.

4. Monitor Interest Rates

Stay aware of market trends—especially as your fixed period nears its end.

Final Thoughts: Is It Right for You?

A Hybrid ARM mortgage in Indiana can be:

- A smart financial tool

- A strategic stepping stone

- Or a risky choice—if misunderstood

At its core, it’s about timing.

If your life plans align with the fixed period, it can work beautifully.

If not, it can create stress.

The Bottom Line

Hybrid ARMs aren’t “good” or “bad.”

They’re situational.

The best borrowers for this type of loan are the ones who:

- Understand how it works

- Plan ahead

- Stay financially flexible

If that sounds like you, it might be worth exploring.