For the men and women who have served our country, coming home should come with opportunity — especially when it comes to owning a home. If you’re a veteran, active-duty service member, or eligible surviving spouse living in Indiana, a VA loan can be one of the most powerful homebuying tools available to you.

Indiana, known for its affordable housing, strong communities, and growing job markets, is an excellent place to plant roots. In this guide, we’ll walk through how VA loans work in Indiana, who qualifies, what benefits you can expect, and how to successfully navigate the process as a Hoosier veteran.

Table of Contents

What Is a VA Loan?

A VA loan is a mortgage backed by the U.S. Department of Veterans Affairs. Unlike conventional loans, VA loans are designed specifically to help veterans and service members become homeowners — often with more flexible requirements and lower upfront costs.

It’s important to note that the VA doesn’t directly lend money. Instead, private lenders (like banks and mortgage companies) provide the loan, and the VA guarantees a portion of it. That guarantee reduces the lender’s risk, which often translates into better terms for borrowers.

Why VA Loans Make Sense in Indiana

Indiana consistently ranks among the most affordable states for housing. From Indianapolis and Fort Wayne to smaller communities like Kokomo or Terre Haute, home prices tend to be lower than the national average. That affordability pairs extremely well with the advantages of a VA loan.

Here’s why many Hoosier veterans choose VA financing:

1. No Down Payment Required

One of the biggest advantages of a VA loan is that eligible borrowers can purchase a home with zero down payment. In a state like Indiana — where median home prices are relatively modest — this benefit can dramatically reduce the barrier to homeownership.

Instead of spending years saving for a 10–20% down payment, you may be able to move forward sooner.

2. No Private Mortgage Insurance (PMI)

Conventional loans often require private mortgage insurance if you put down less than 20%. VA loans do not require PMI, even with zero down. This can save Indiana veterans hundreds of dollars per month.

3. Competitive Interest Rates

Because the loan is backed by the VA, lenders typically offer lower interest rates compared to conventional mortgages. Over the life of a 30-year loan, even a slightly lower rate can mean significant savings.

4. Flexible Credit Requirements

While lenders still evaluate credit scores and financial stability, VA loans tend to have more flexible credit standards than conventional financing. This can be especially helpful for veterans transitioning from military service to civilian life.

Who Is Eligible for a VA Loan in Indiana?

VA loan eligibility is based on service history. Generally, you may qualify if you are:

- An active-duty service member

- A veteran who meets minimum service requirements

- A member of the National Guard or Reserves

- An eligible surviving spouse of a service member who died in the line of duty or as a result of a service-connected disability

To move forward, you’ll need a Certificate of Eligibility (COE). Most lenders can help you obtain this document quickly, often electronically.

VA Loan Limits in Indiana

In recent years, VA loan limits have changed significantly. If you have full entitlement, there is technically no loan limit — meaning you can borrow as much as a lender is willing to approve without a down payment, as long as you qualify financially.

However, lenders will still consider your income, credit, debt-to-income ratio, and overall financial picture when determining how much you can borrow.

In higher-cost Indiana areas like Carmel or parts of the Indianapolis metro, this flexibility can be especially valuable.

The VA Funding Fee

While VA loans eliminate PMI and down payments, they do include a VA funding fee. This one-time fee helps keep the program running for future veterans.

The funding fee varies based on:

- Whether this is your first VA loan

- Your down payment amount (if any)

- Whether you’re active duty, Reserve, or National Guard

The good news? Many veterans with service-connected disabilities are exempt from paying the funding fee altogether.

The fee can also be rolled into the loan amount instead of paid upfront.

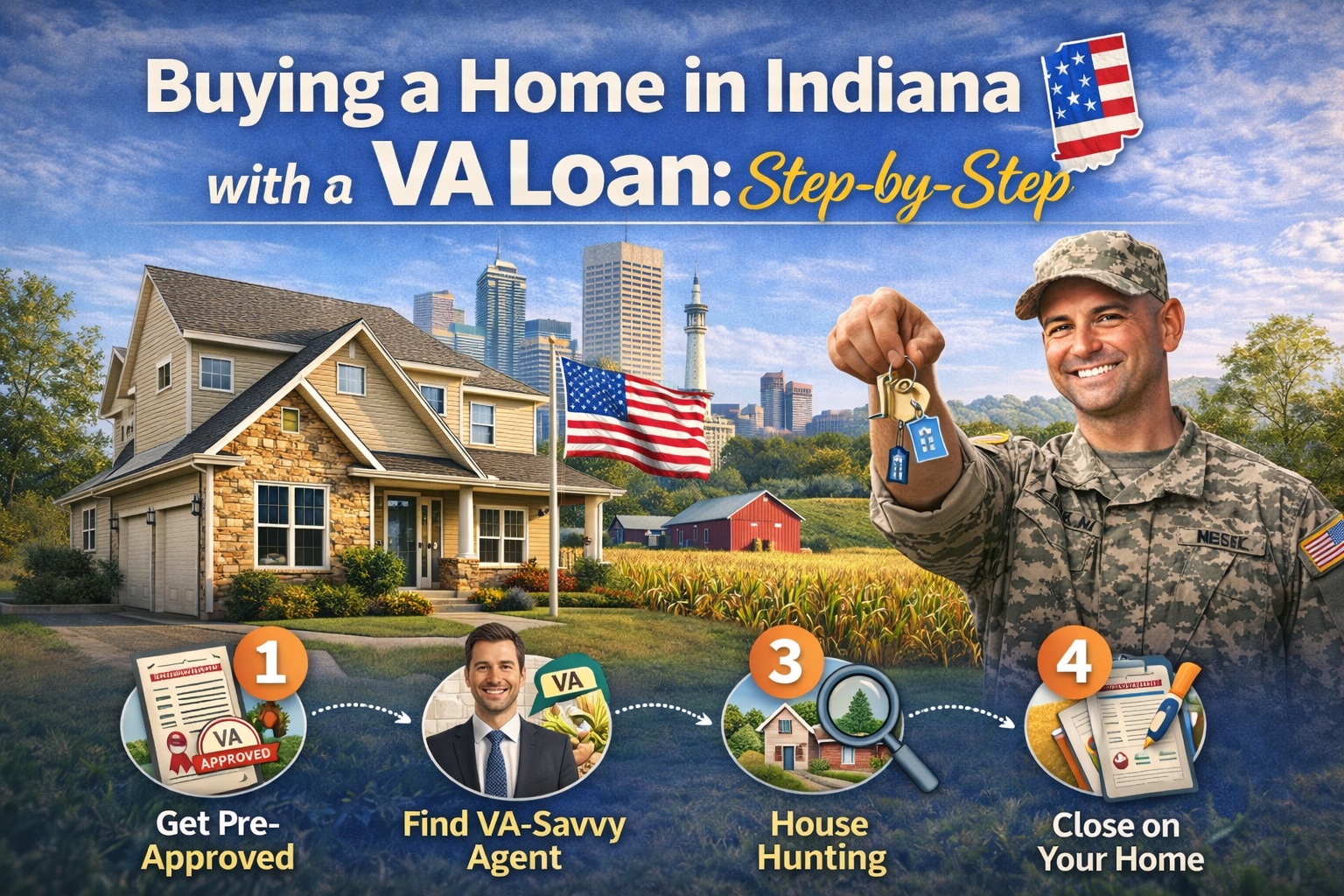

Buying a Home in Indiana with a VA Loan: Step-by-Step

If you’re ready to move forward, here’s what the process typically looks like:

Step 1: Get Pre-Approved

Before shopping for a home in Indiana, meet with a VA-approved lender to get pre-approved. This helps you understand your budget and shows sellers you’re a serious buyer.

Step 2: Find a VA-Savvy Real Estate Agent

Working with an agent who understands VA loans can make a huge difference. VA loans have specific appraisal and property condition requirements, so experience matters.

Step 3: House Hunting

Whether you’re looking for a quiet home in rural Indiana or something closer to downtown Indianapolis, your agent will help you find properties that meet VA standards.

Step 4: VA Appraisal and Underwriting

Once your offer is accepted, the lender will order a VA appraisal. This ensures:

- The home is worth the purchase price

- The property meets VA minimum property requirements

These standards are designed to protect veterans from purchasing unsafe or structurally unsound homes.

Step 5: Close on Your New Home

After underwriting approval, you’ll move to closing — where you sign final paperwork and receive the keys to your new Indiana home.

Can You Use a VA Loan More Than Once?

Yes. VA loans are not a one-time benefit.

You may be able to:

- Reuse your VA loan benefit after selling a previous home

- Use remaining entitlement for a second home purchase

- Refinance an existing mortgage with a VA Interest Rate Reduction Refinance Loan (IRRRL), often called a VA streamline refinance

This flexibility is especially helpful for military families who relocate frequently or veterans upgrading homes as their families grow.

Common Myths About VA Loans

Despite their advantages, VA loans are often misunderstood. Let’s clear up a few myths:

Myth #1: VA loans take too long to close.

In reality, VA loans often close just as quickly as conventional loans when handled by experienced lenders.

Myth #2: Sellers don’t like VA loans.

This misconception usually stems from misunderstandings about appraisals. In competitive Indiana markets, a strong offer backed by a solid pre-approval can absolutely compete.

Myth #3: VA loans are only for first-time buyers.

Not true. You can use your VA benefit multiple times.

Special Considerations for Indiana Veterans

Indiana is home to several military installations and veteran communities, including Grissom Air Reserve Base and Camp Atterbury. Local lenders and real estate professionals are often very familiar with VA transactions.

Additionally, Indiana offers property tax deductions for disabled veterans, which can further reduce the cost of homeownership. Be sure to check with your county assessor’s office to see what benefits may apply to you.

Final Thoughts: A Well-Deserved Benefit

Serving your country is a tremendous commitment. The VA loan program is one way the nation says “thank you” — by making homeownership more accessible and affordable.

For Hoosier veterans, the combination of Indiana’s affordable housing market and the powerful advantages of VA financing creates an exceptional opportunity. Whether you’re settling down after active duty, relocating within the state, or buying your very first home, a VA loan can help you move forward with confidence.

If you think you may be eligible, the best next step is speaking with a VA-approved lender who understands the Indiana market. With the right guidance, your path to owning a home in the Hoosier State could be closer than you think.